The cryptocurrency exchange founded by the Winklevoss twins is facing a severe downturn following its public market debut. Bloomberg has issued a stark warning, suggesting the company is headed for a ‘hard landing’ after a turbulent period of restructuring. This transformation requires significant time and capital, leaving little margin for error in a hostile market environment.

In September 2025, the platform made its move to the Nasdaq stock exchange. The initial public offering was priced at $28 per share for 15.18 million Class A shares. This pricing exceeded the initial target range of $24 to $26, successfully raising $425 million in capital. At its peak valuation, the company’s market cap hovered close to $4 billion.

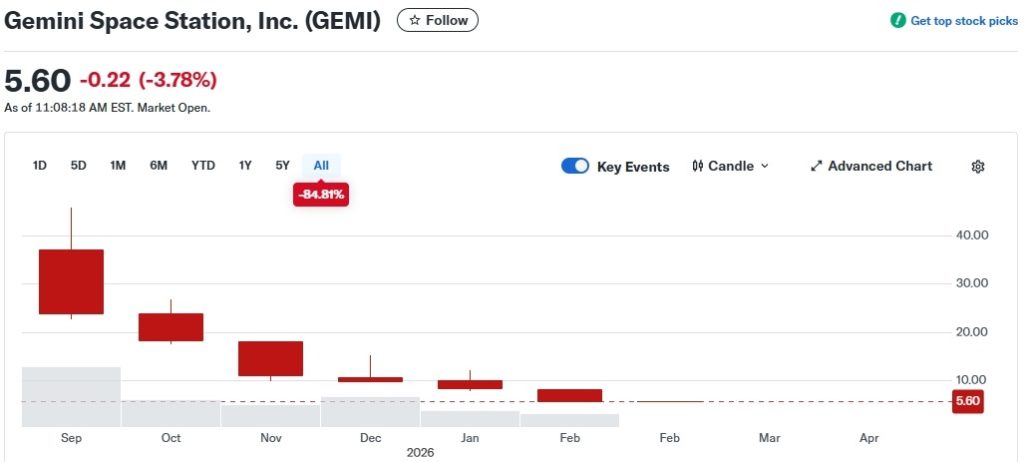

However, the stock performance since that debut has been nothing short of disastrous. As of the latest data, the market capitalization has collapsed to $661.5 million. This represents a staggering decline of nearly 85% from its peak. The ticker GEMI has consistently closed lower on a monthly basis, reflecting deep investor pessimism.

Operational cuts began in early February with the announcement of a 25% workforce reduction. Simultaneously, the exchange decided to withdraw its services from the United Kingdom, the European Union, and Australia. Shortly after, the company saw a shakeup in its upper management, parting ways with CIO Marshall Beard, CFO Dan Chen, and General Counsel Tyler Mead. Bloomberg also reported that the exchange quietly trimmed its United States staff further.

Analysts from Truist Securities, including Matthew Coad, Lucas Ramadan, and Cameron Macleod, identified the core of the problem. They stated that Gemini’s leadership made a significant miscalculation by betting heavily on the crypto market’s continued growth through 2027. Instead, digital asset prices collapsed, leaving the exchange exposed. The firm has historically struggled to capture a dominant market share, and that lag has only intensified.

Recent data highlights this struggle. In January, Gemini’s share of the spot crypto trading market was just 0.1%. This is a sharp decline from an already underwhelming 0.6% recorded in June 2025. Analyst Coad emphasized that a fundamental change in strategy is required for survival.

A Pivot to New Verticals

With trading revenues in decline, co-founders Cameron and Tyler Winklevoss have signaled a major shift in business focus. The company is moving away from a pure-play exchange model to diversify its revenue streams. The new roadmap prioritizes the development of a platform for prediction markets, enhanced custodial services, and the issuance of credit cards.

Geographically, the exchange is retreating to its strongestholds. Future trading operations will focus exclusively on the United States and Singapore. In a move to streamline operations, Gemini decided not to hire a new chief operating officer. Instead, Cameron Winklevoss has absorbed some of those responsibilities directly.

The brothers admitted that their international expansion efforts proved more difficult than anticipated. The company became overburdened by increased organizational and operational complexity, which drove costs higher. Despite these setbacks, Tyler Winklevoss expressed a contrarian view on social media, stating that the sentiment in the crypto market is so poor that he feels quite optimistic.

This optimism has been met with skepticism from the community. Observers noted a contradiction between Tyler’s bullish public statements and the actions of the Winklevoss Capital wallet. On-chain data tagged by Arkham shows a continuous sell-off of Bitcoin over the past year. The wallet balance has dropped from approximately 23,000 BTC to around 11,000 BTC. This is a stark contrast to the peak holdings of roughly 108,000 BTC stored in 2014.

Liquidity Concerns and Financial Pressure

The financials paint a challenging picture for the restructuring effort. For the fiscal year 2025, Gemini reported expected net revenue of $175 million. This stands in stark contrast to total operating expenses of $530 million. At this rate of cash burn, the $425 million raised during the IPO does not appear to be a substantial reserve for the long term.

The company’s public listing paradoxically complicates raising additional funds. Shareholders, already unhappy with the stock’s precipitous decline, fear further dilution of their stakes. This makes a secondary offering difficult to execute without crashing the price further.

Analyst Matthew Coad believes that cash injections from the founders are a likely scenario to keep operations running. Given that the brothers remain deeply involved, they may need to inject personal capital to bridge the gap. However, Coad also acknowledged that investors have valid reasons to question the company’s solvency.

Adding to the pressure, the company recently settled with the US Securities and Exchange Commission. The lawsuit, filed two years ago, centered on the now-defunct Gemini Earn product. While the legal threat has been resolved, the reputational and financial costs of the settlement add to the burden of the current turnaround plan.